3 Things Founders Might Miss When Starting Their Lending Business

May 15, 2023

South and Southeast Asian financial startups are expanding their customer offerings through end-to-end financial services, which they believe will lead to profitability.

One notable trend in the fintech industry in South and Southeast Asia is the move towards becoming a full-stack financial service provider, which often also includes expanding to lending products to diversify and retain customers.

In response, some regulators in the region have introduced new policies (e.g., Indonesia’s POJK 10 which requires lenders to have USD $1.6M paid up capital) to heighten transparency and weed-out unsafe lending practices. This, combined with rising interest rates and some high-profile legal troubles at existing lenders, have made firms more cautious about entering the space.

However, we believe it is possible for fintechs to sustainably and successfully expand to lending products, if they avoid these three common pitfalls.

1. Incorrectly Incentivizing Your Salesforce

Lending businesses are currently facing challenges from increased capital costs and reduced customer demand for loans as interest rates climb. Therefore, many startups are seeking to increase disbursements or expand their geographical reach to achieve profitability.

To do this, an incentivized salesforce is necessary, but it is important to calibrate these incentives appropriately. In the unsecured lending space, we’ve seen a growing number of fraudulent loans as salespeople have taken advantage of arbitrage opportunities.

They might disburse loans to themselves or friends to increase their distribution numbers. We see this happen most often when companies offer high commission rates for new loan distributions. Salespeople may also collude with borrowers or steal identities to commit fraud by taking out loans with no intention of repayment.

To mitigate the risk of salesperson fraud and loan arbitrage, companies can adjust their incentive structures to align with non-performing loan (NPL) targets and tie commissions to successful repayment.

This discourages salespeople from bypassing underwriting processes and encourages responsible lending practices. Additionally, management can monitor sales cohorts for any signs of collusion or fraud, closely tracking delinquent loans (< DPD 30+) to quickly identify and address any emerging trends.

2. Failing to Integrate and Layer Collections

Disbursements are a popular metric for lending businesses to showcase growth, often overshadowing the importance of a well-designed collection model. In today’s lending environment, where the ability to collect back loans is critical, focusing solely on speedy disbursements is no longer sufficient.

While having a collection team is necessary, it is not enough to ensure low levels of non-performing loans (NPLs). The way in which collections are handled is equally important, as it can significantly impact the amount of revenue lost due to defaulting borrowers.

In 2022, some SSEA startups that focused efforts on disbursements to bolster their GTV (Gross Transaction Volume) and other gross metrics neglected investing in their collections. As a result, some of these firms faced increased provisioning expenses that exceeded their net interest revenue for certain customer groups. This led to a knee-jerk reaction of raising interest rates to cover potential losses, resulting in increased customer churn.

Moreover, some companies failed to review their external debt collections partners and prioritized cost savings over effective collections practices. In some cases, debt collectors resorted to unorthodox/illegal methods, causing company reputational damage.

Integrating Collections

Expanding lending startups often adopt a downstream collections structure, where the collection team handles all lending products. However, this structure creates slow response loops for iterating and changing risk classifications, leading to miscommunication between collections, product, and risk teams.

A product-led structure, where collections report directly to the product head (such as MSME loans), solves this issue for maturing startups. This structure fosters more ownership and communication between the collections team and the rest of the team, enabling product leads to spot trends and intervene quickly.

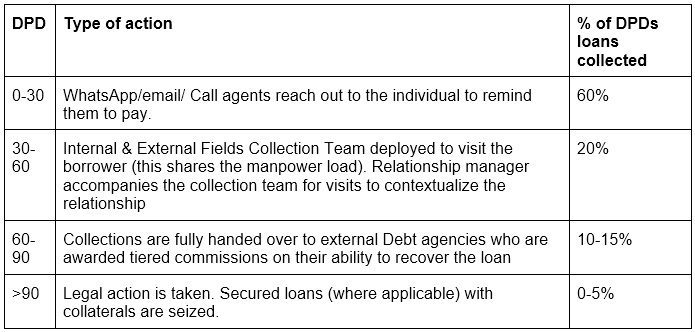

Managing Days Past Dues+

Below is an example of how a leading lender in SEA layers its collection process.

The lending startup categorizes lenders by their risk level (Low, Medium, High) and applies different interactions for maximized effort before the day past due (DPD).

Once the DPD begins, the lender applies a standard treatment across the groups. Doing a pre-DPD action plan helps to reduce NPLs and allows the team to anticipate potential NPLs before they happen. It also ensures that the same process is applied to all lenders, and avoids preferential treatment or unpalatable approaches to collection.

Once the DPD is triggered, the firm then deploys call agents to call and obtain a commitment for repayment, with the call being recorded.

3. Forgetting That NPLs Aren’t the Full Picture for Managing Risks

Nonperforming loans (NPLs) are an important risk metric for lending businesses, but they can understate the risk levels if taken one dimensionally. High NPLs lead to reduced net interest income, additional capital requirements, lower ratings, and increased funding costs.

Since NPLs are a lagged indicator, businesses often can’t iterate on their underwriting and collection strategies until after a significant amount of time has passed since disbursements. This can be a costly lesson for new lending products if mismanaged. Additionally, if the business is too conservative and considers all non-performing loans as any loan due past day 0 (DPD 0+,) it could stifle lending innovation.

Founders must be aware of the risk level of NPLs, prepare for them in advance, and identify user actions that lead to NPLs. Lending experts have noted that some startups’ lending teams use an ambiguous definition of NPLs, potentially manipulating the definition to avoid categorization. Founders must clearly understand how NPLs are defined, including the multiple exceptions that can result in an overestimation of risk.

To manage risk while scaling, startups should anticipate and provision for net loan loss, creating a feedback loop between underwriting, product, and collection teams – this will ensure that products are priced properly. A tiered NPL provisioning policy should be implemented, with provisioning increasing as Days Past Due (DPD) increases and adjusted based on interest rate changes. Not provisioning until a loss occurs weakens the feedback loop.

Finally, identifying user behavior that results in NPLs is a crucial element in managing risks as NPLs are a lagging indicator that leaves the lender with fewer options to correct the situation and help the borrowers.

To address this issue, some fintech companies analyze user behavior on their platforms, such as behavior seeking new credit line options or frequently checking outstanding loan balances. In addition, some SEA lenders utilize API monitoring tools with credit scoring companies to flag any other distressed loans that the borrower may already start defaulting on.

By monitoring app or platform usage, relationship managers can engage borrowers before payment deadlines. Consequently, this facilitates early loan restructuring or alternative solutions for borrowers, improving the management of potential risks.

Avoiding Pitfalls

Fintech companies often view lending as a low-hanging fruit for diversifying and scaling up their full-stack value proposition.

When executed correctly, it can create a powerful product flywheel. However, lending can be a risky business. Avoiding these three pitfalls, drawn from various founders’ experiences, can help ensure a successful entry into the lending ecosystem.

If you have any questions or would like to explore this area further, don’t hesitate to get in touch with us!